What the law change does

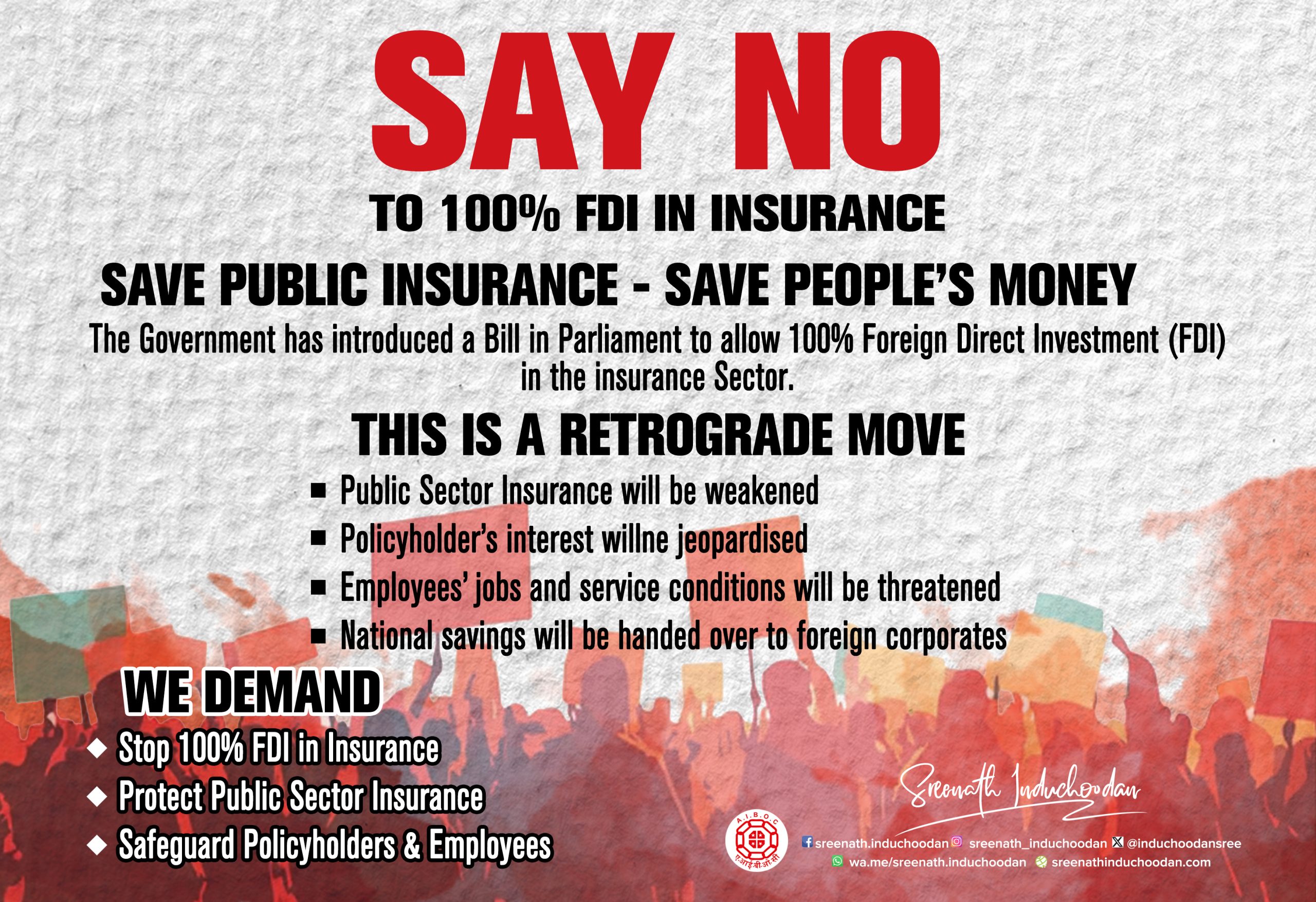

Parliament has approved a Bill in December 2025 that raises the permitted foreign direct investment (FDI) in Indian insurance companies from 74% to 100%. The Government says the step aims to bring more capital, products and technology into the sector. But why 100% FDI in Insurance undermines India’s constitutional mandate for a welfare-state.

How foreign insurers operate in India today

Since liberalisation, foreign insurers have entered India by setting up licensed Indian insurers typically joint ventures with Indian partners. The sector’s FDI cap rose in stages (26% → 49% → 74%) to allow greater foreign participation while keeping an Indian-controlled entity framework; many private insurers today are structured as Indian companies with foreign parent shareholding and bancassurance/agency tie-ups. Raising the cap to 100% removes that structural requirement.

Constitutional philosophy: India as a welfare state and the Directive Principles

The Constitution, through its Preamble and Part IV, declares the goals of social, economic, and political justice. Also, it directs the State to promote the welfare of the people and to minimise inequalities in income, as reflected in the Directive Principles of State Policy, including Articles 38, 39, and 41.While DPSPs are non-justiciable, they are binding in governance and form the constitutional framework for social welfare policy. Policies that systematically reduce State capacity to secure social protection or concentrate control of social-security institutions are therefore in tension with the Constitution’s welfare commitments.

The Constitution of India does not envisage the State as a passive market facilitator but mandates it to function as a welfare State, actively intervening to secure social and economic justice. This vision is not rhetorical; it is firmly embedded in the Directive Principles of State Policy. These principles obligate the State to ensure social security, equitable distribution of resources, and protection of vulnerable citizens.

In this framework, insurance is not a mere financial product—it is a social guarantee.

Why 100% FDI threatens the welfare-state objectives

a. Weakening public control over a social-security instrument

Insurance life, health, crop, disaster cover and pension-related products — is not merely a commercial market: it is a tool for social protection and long-term savings. Accordingly, full offshore ownership and control reduce the State’s ability to shape sectoral objectives toward inclusion, cross-subsidy, and national priorities.

b. Profit repatriation and loss of domestic long-term savings

Full foreign ownership makes repatriation of profits/dividends and foreign exit more likely. Insurance collects long-term domestic savings; if returns are channelled abroad, national capital formation and funding options for public projects may suffer.

c. Commercial priorities can crowd out social goals

Foreign parent firms answer to shareholders and global profit targets. This risks shifting insurance products toward high-margin urban and affluent customers, at the cost of rural, informal, and vulnerable groups whom the Constitution obliges the State to protect.

d. Systemic and sovereignty risks

In crises a foreign owner may withdraw capital or restrict operations in ways that harm policyholders and financial stability. Critical financial infrastructure remaining under national control is a constitutional and sovereign interest.

e. Impact on public insurers and public-sector character

Public insurers and public-sector banks have historically played counter-cyclical, developmental roles (supporting infrastructure finance, government savings mobilization and social schemes). Full foreign control in insurance will erode that public-sector buffer and accelerate market concentration under global corporate owners.

Wherever possible, we should judge these consequences against empirical evidence and international comparisons, but the risk direction is clear: structural changes in ownership alter incentives, governance, and policy space.

What the “present rule” was and why the change matters practically

Before this amendment, the FDI in Insurance cap stood at 74% (an increase from earlier levels). That 74% cap still meant the Indian entity structure, regulatory conditions, local boards and on-the-ground Indian operations constrained unilateral foreign control. Moving to 100% FDI removes that guardrail and allows foreign firms to own and directly control Indian insurers without the same structural constraints.

Practical consequences

- Loss of public purpose: Insurance is a public-interest instrument; full foreign control risks prioritising shareholder returns over social protection.

- Erosion of public-sector buffers: Today’s step sets a precedent, if insurance can be fully foreign-owned, other strategic public assets could be next.

- Jobs and conditions: Foreign ownership frequently brings restructuring, contractualisation, offshoring of functions and pressure on wages/benefits.

- Policy space: The State must retain the ability to direct sectoral priorities (rural penetration, price control for essential schemes, cross-subsidies).

- Regulatory risks: Even with stronger regulator powers on paper, effective enforcement in episodes of foreign exit or global stress is difficult.

Why Trade Unions Oppose 100% FDI

- It privatises profits and socialises risks

- It weakens public sector institutions

- It undermines job security and service conditions

- It reduces national control over strategic financial sectors

- It is part of a broader agenda of diluting public ownership and public accountability

Why Public Sector Bankers Must Oppose This

Today it is insurance; tomorrow it will be banking.

Public sector bankers know from experience how gradual policy changes lead to dilution of public ownership, erosion of autonomy, increased privatisation and loss of the developmental role of PSBs.

All in all, if strategic sectors are handed over to foreign capital, the public sector character of India’s financial system will be irreversibly weakened. What we lose is not just ownership—but economic sovereignty, employment security and social responsibility.

Conclusion

100% FDI in insurance is not a reform—it is a retreat from national interest.

As can be seen, trade unions, public sector employees and citizens must collectively oppose this move. We should protect public institutions, safeguard policyholders and preserve the public sector character of India’s financial system.

“The Preamble and Directive Principles commit the State to social and economic justice. Structural reforms that divest control of social-security instruments to foreign capital must meet that constitutional test and until they do, public-sector bankers and trade unions must oppose 100% FDI in insurance.”